# 08 - Enough Due Diligence to put in an Offer

Due diligence is simply the information you need to gather to confidently buy a property. There's free information, paid reports, easily accessible websites, and professionals who can help.

I'm splitting the due diligence period into two parts:

- Up to putting in an offer

- Under contract, but before you confirm the purchase

In this issue I'll cover what you need to know before you put in your offer.

Like a lot of things in property investing, this comes back to your risk profile and your intended outcome for the property.

At the most basic level, your due diligence could be: "Do I have enough money to buy this deal?" — and that's it.

I wouldn't be that cavalier, and I wouldn't suggest it for you either. But what you need to know will genuinely differ from person to person — based on your experience, your risk profile, where you are in your property journey, and what you plan to do with the property.

What's important to remember is that almost anything in your offer can be changed during the due diligence period. Price, deposit, settlement dates, purchasing entity — all of these can be adjusted based on what you discover. The vendor can refuse your changes, of course, but this period is your opportunity to find out as much as possible before you go unconditional and absolutely commit to buying.

The 5 Things You Need to Know Before You Make an Offer

1. Price — How much should you be paying?

There are two things to think about here: what is the property worth right now, and what is its potential value to you based on what you intend to do with it. The first is easier to quantify. The second is more subjective.

For current value — comparable sales near the property are the most reliable way to find this out. What has recently sold nearby that is similar? Ask the listing agent, but be aware of their potential bias. Ask other agents too.

For potential value — think about your intended outcome (see #2 below). Do you own a neighbouring property? Do you know about an upcoming zone change? Why is this property more valuable to you than to another buyer — and what is that potential worth?

Free websites: homes.co.nz · oneroof.co.nz · realestate.co.nz · propertyvalue.co.nz · qv.co.nz

2. Outcome — Does this property suit your intended strategy?

I talk a lot about adding value. Knowing what you can do with a property massively affects what you should offer for it. Are you going to flip it? Subdivide it? Renovate to create positive cashflow and hold long term? Could it work as an Airbnb? Is there a commercial angle? Could a multi-unit property be split into individual titles?

You need to know enough about the zoning, tenant desirability, post-reno value, land density, and renovation costs to understand which value-add options are available to you — and which ones actually make sense.

Having multiple options is great, but usually 1–2 will stand out as the strongest. Research quickly. In property, speed wins.

Free websites (Christchurch-specific, but your region will have equivalents): canterburymaps.govt.nz · districtplan.ccc.govt.nz · ccc.govt.nz

For other regions, search "[your region] council GIS map." Zoning tells you what you can legally do with the land.

Not sure what work needs building consent? Download my free No Consent Renovation Guide.

3. Finance — Can you get the money to buy this property?

You don't need this 100% confirmed before putting in your offer, but the earlier you know, the better. Ideally, you'll be pre-approved before you even start searching.

Think about where your money is coming from: deposit, purchase price, renovation costs, and other expenses. Cash, usable equity, vendor finance, bank loans, second-tier finance, a JV finance partner?

Your deposit doesn't need to be the standard 10%. My aim is 3–4% to cover fees — and it can be as low as $1.

When you're confident about your finance, you can reduce your due diligence conditions, make a faster offer, and become a far more attractive buyer to the vendor — especially important in a competitive market.

Good mortgage advisors to help you: Lighthouse Financial · Mortgage Life · Guardian Smith

4. Condition — What shape is the property in?

I'd recommend most people get a builder's report — but it doesn't need to happen before your offer. At $500+, you'd ideally have the property under contract first before booking and paying for one.

What you can do right now, at the open home, is a solid visual check that tells you whether the property is worth pursuing at all. Here's what to look at:

Water & drainage

- Check under all sinks and vanities for signs of leaks or moisture

- Check around all showers, toilets, and plumbing fixtures

- Turn on all the taps — kitchen, bathroom, laundry. How's the pressure? Does it drain away cleanly?

- While the taps are running, step outside and check the gully traps to make sure wastewater is flowing away properly

Electrical

- Are the plugs and switches old-fashioned or modern? Old can mean expensive.

- What does the switchboard look like? Modern circuit breakers are ideal.

Paint & flooring

- Inside and out — look for peeling, bubbling, or mouldy surfaces

- Check carpet and vinyl for lifting, wear, or odour

Structure & exterior

- Insulation — ceiling and underfloor is required by law for rentals. You can check these if you're willing.

- Walk the floors. Without a laser level it's hard to be precise, but you can feel for obvious unevenness.

- Gutters — are they overflowing, growing weeds, or leaking? A visual from the street tells you a lot.

- Stormwater — does it drain away from the property? A hose can help you check.

Finding issues doesn't mean you shouldn't make an offer. Due diligence is simply about understanding what you're buying. If there are problems — and there usually are in older homes — ask yourself: can they be fixed? What will it cost? Will these affect your ability to rent or sell?

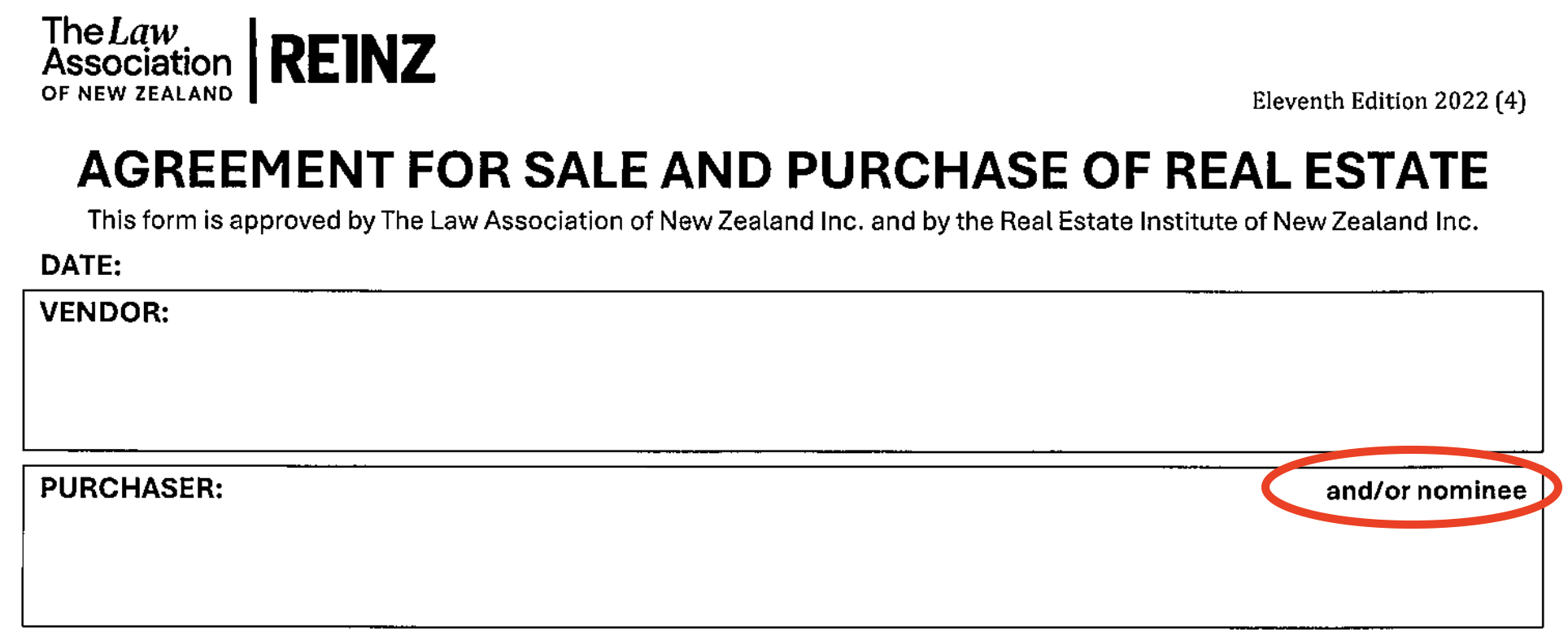

5. Entity — Who is buying this property?

Like finance, you don't absolutely need to have this sorted before you put in an offer — as long as you leave the "and/or nominee" clause intact on the contract, you can change the eventual purchaser later.

But your intended outcome should guide this decision. Planning to flip? A GST-registered company may be the right structure. Long-term hold? A trust or personal name might suit better.

If you need to set up a new company, do it before you start making offers — you can't set one up after the fact and put the purchase in its name.

Those are the 5 areas to work through before you make an offer. All the steps above are FREE. Just costing you some time to work through.

Some investors want to know everything before they move. Others won't even need to visit the property in person.

When I look at a property, I focus on price and condition first. I want to figure out my end goal asap and what it will cost to get there.

Once you can work through these 5 areas quickly, you'll enough information to make a confident offer.

I'll cover secondary due diligence in a future issue — that's the deeper work you do once the property is under contract and you're deciding whether to go unconditional.

To help you put this into practice, I've put together a free 25-point Due Diligence Checklist — take it to your next open home and tick the boxes as you go.

If you want 1:1 help with putting in your offer, your due diligence - or any part of your property investing journey have a look at my 1:1 Strategy Session

Part 2 coming soon — The Due Diligence needed before you confirm the contract

Ready to invest smarter?

Join 800+ New Zealanders getting straight-talking property advice every week.

Free. No spam. Unsubscribe anytime.